Modeling the 2008-2009 Financial Meltdown Using Metastable State Phase Transitions

Now that we've weathered the crisis of 2008-2009, we can prudently ask ourselves: "What are the warning signs of imminent meltdown? How can we predict - and act prior to - a major market collapse?"

This post continues the theme begun in the previous post, of playing with a not-quite Gedanken experiment; looking for a useful model that explains what happened with the U.S. financial system at the end of 2008 and early 2009.

The important contribution of this post is that it presents a graphical representation of a model (free energy from statistical thermodynamics) that allows a system to be in a metastable state. This would characterize the overall banking/private equity/leveraged buy-out industry in 2008, just prior to the meltdown.

The following Figure 1 shows a "reduced" (parameter-normalized) free energy F* as a function of x, where x can range from 0 to 1. (For the free energy equation, and discussion thereof, see Phase Spaces: Mapping Complex Systems.

Figure 1: Set of five free energy graphs; F* versus x, where F* is the "reduced" (re-parameterized) free energy, and x represents the fraction of units in the system in an "on" or "activated" state. The five different graphs are obtained for different combinations of enthalpy parameters (to be discussed in a following post). The topmost graph refers to Region A (see following Figure 2), in which only a single free energy minimum exists, and is for a low value of x. The middle three graphs are for parameter values taken from Region D of Figure 2; these allow for double minima to appear. That means that a system can be in either a low-x or high-x state. (Relatively few activated units, or almost all units active.) The lowest graph corresponds to Region F, for which only a single free energy minimum exists, but this time with a high value of x (most units are "active" or "on.")

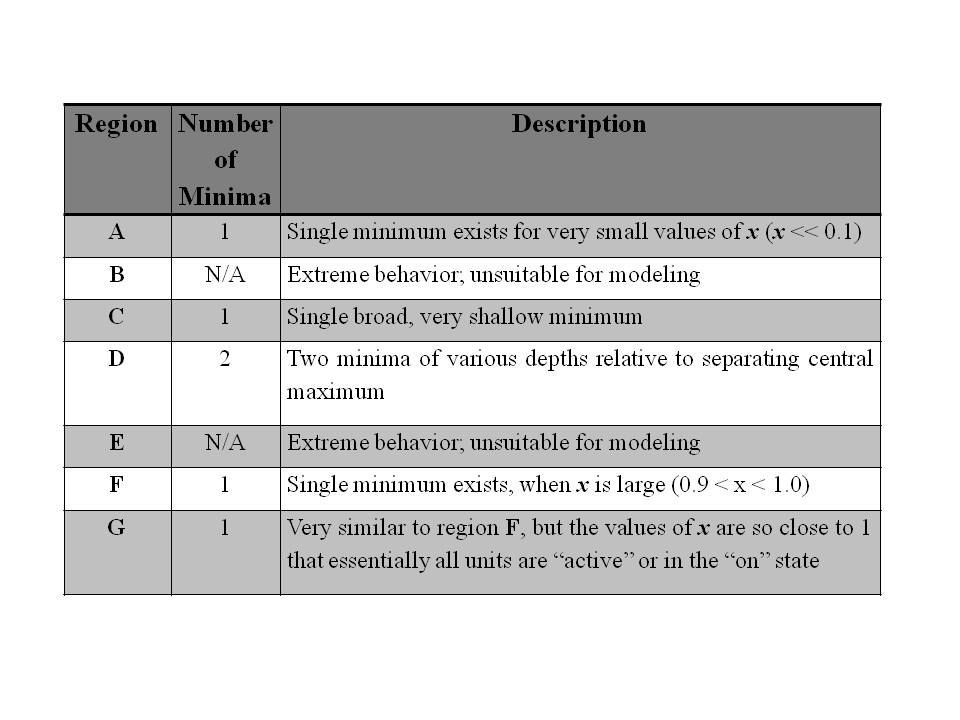

For reference, Figure 2 reproduces the phase space for different types of free energy graphs, originally presented and discussed in Phase Spaces: Mapping Complex Systems. Table 1, which summarizes the characteristics of these different regions, was also presented in that post.

Figure 2 shows a phase space of seven distinct regions, labeled A-G. These regions are characterized in the following Table 1.

Table 1: The regions identified as A-G in the preceding Figure 2 are characterized in terms of number of (reduced) free energy minima, and whether these minima correspond to low, high, or both low and high values of x.

The important thing about this Figure 2 phase space diagram, and the distinct regions within it, is that it shows how a phase transition could happen between two very different states in a system; one where x is high (most units are in a very active or "on" state x=> 1), and another in which x is low (most units are in an inactive or "off" state, x=>0).

To see this possibility, please go to the discussion presented in Phase Spaces: Mapping Complex Systems.

The important previous blogpost references for this post are:

1) Some statistical thermodynamics theory (basic Ising spin-glass theory, with interacting bistate units), established in Phase Spaces: Mapping Complex Systems, and

2) Chasing Goldman Sachs, by Suzanne McGee, discussed in the previous post, Modeling a Financial Nonlinear Phase Transition.

As a starting point, I am using the basic Ising model development outlined by Goldenfeld in his Lectures on Phase Transitions and the Renormalization Group, as well as a paper by Pelizzola that describes the Cluster Variation Method (CVM) in relation with graph theory.

The core idea that I will use for this discussion is that at the time of the meltdown, the various "key players" were in a highly metastable state.

In nature, it is common for systems to "tend towards equilibrium." This means that they seek a balance between enthalpy (the energy associated with each component of the system) and entropy (the tendency of a system to move towards greatest possible dispersal among all possible energy and association configurations).

A systems's free energy (F) represents the dynamic tension between the two factors of minimizing overall system enthalpy and maximizing overall entropy. When free energy is at a minimum, we say that a system is in equilibrium.

Often, in nature, when conditions change, a system will adjust its composition to keep its free energy at a minimum (to stay in equilibrium). However, not all systems can respond adequately, even when the conditions under which they are operating change substantially. Instead, they sometimes go into a metastable state; a state which is locally a free energy minimum, but not the true, overall free energy minimum. However, the system will persist in this metastable state until conditions change so much that the little, local free energy "well" which it was inhabiting disappears completely. Then, it has no recourse. It will slide into its true "minimal free energy state," that is, it will move into equilibrium.